For so many years, that’s how it was for the U.S. hotel industry in terms of business mix. Every...

Published Articles

A Variable Recovery The pandemic and subsequent economic impact and shock the hotel industry experienced has varied widely by market and submarket type within markets. Hotel type and historical business mix has played a significant role in how well a property fared throughout 2020, 2021 and 2022, which is likely to become our next baseline normal year for industry comparisons.

An important lesson the industry has learned time and again throughout the last 36 months has been to be patient and nimble. Anticipating performance has, and will continue to be, difficult. One primary reason for this has been the major shift in business mix between commercial and leisure.

Kalibri Labs has been tracking a set of metrics called the Commercial:Leisure Index for a year, starting in the summer of 2021 when we witnessed U.S. Guest Paid ADR surpass 2019 performance for the first time. This metric examines U.S. lodging performance by aggregating demand by the rate category used to book an overnight stay, and identifying the booking as either commercial or leisure.

For the purposes of this index comparison we’ll use the following definitions:

Commercial transient:

Corporate, government, consortia, rack/BAR (Sun-Thurs), and loyalty member rate (Sunday-Thursday).

Commercial group:

Association, convention, corporate, government, contract/crew.

Leisure transient:

AAA/AARP, advance purchase, friends and family, promotion/packages, loyalty redemption, rack/BAR (Fri-Sat), loyalty member rate (Fri-Sat), and OTA.

Leisure group:

SMERF and tour/wholesale.

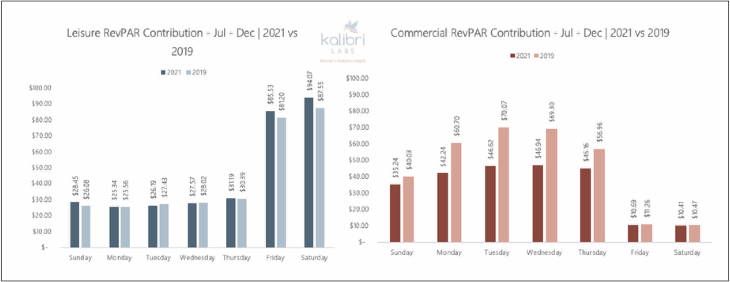

Thursday is the New Friday: How Leisure Impacted 2021

In August 2021, Kalibri Labs anticipated the industry might experience a weakening of leisure demand, due to most schools in the U.S. returning to classroom learning and the impact of the Delta variant (and later, Omicron). It was also suggested the pent-up demand for leisure travel was likely to have been exhausted by the end of summer.

However, this thinking was proven wrong. More travelers than ever hit the road and stayed overnight in hotels from Thursday through Sunday, mainly in leisure segments. The impact of this continued leisure travel throughout the second half of 2021 had an extremely positive impact on Guest Paid RevPAR and Guest Paid ADR from July through December. It also helped lift occupancy to more normal levels vs. 2019.

With more and more people able to work from anywhere, the industry is continuing to experience an increase in Thursday through Sunday stays. This led to an increase in Guest Paid RevPAR contribution for leisure segments on these days of the week, though levels remained relatively flat Monday, Tuesday and Wednesday nights vs. 2019. In comparison, commercial Guest Paid RevPAR contribution decreased all seven days of the week in the second half of 2021 vs. 2019.

Leisure Remains a Gift in the Present

Through March 2022, commercial Guest Paid RevPAR contribution still lags the same time period in 2019 by more than -15%. Leisure is up +1%, driven primarily by strong Guest Paid ADR, up +8.7% for leisure. Given the historic high ADRs the industry witnessed in 2019, this surge in Guest Paid ADR from leisure is truly remarkable, especially since it’s happening throughout the week and across all markets and submarket types.

In March 2022, growth in Guest Paid RevPAR contribution drove markets like Sarasota, Fla.; Flagstaff/Prescott, Ariz.; and the Colorado West Area, which includes areas like Durango and Telluride, into the Top 10 Markets. Because it was the home base for truckers participating in the Washington, DC, trucker convoy at the start of the year, Hagerstown, Md., also jumped into the Top 10 Markets for leisure and commercial occupancy contribution — evidence that mixed-use stays can impact both leisure and commercial segments.

Year to date, Guest Paid RevPAR contribution from leisure is driving above-2019 performance in most chain scales and location types in the U.S. Upper tier hotels in Resort/Destination locations are performing very well, with just Luxury, Upper Upscale, and Independent hotels still trailing 2019 in leisure contribution in urban markets. The market types where hotels in these chain scales are most commonly found are also still underperforming 2019 Guest Paid RevPAR contribution in leisure (specifically large metro urban areas). Meanwhile, we find Resort/Destination, Rural Area/Interstate, and Small City/Town market types all benefitting from the continuing surge in leisure contribution.

Through the Looking Glass: What’s Ahead

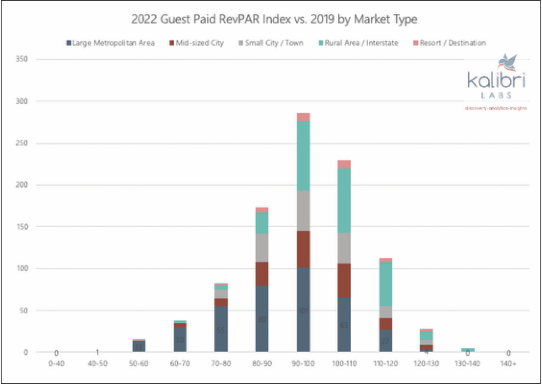

Kalibri Labs tracks performance for 975 submarkets in the U.S., broken out by market type, with examples from large metropolitan areas (i.e., Chelsea in New York City and Fisherman’s Wharf in San Francisco) to small city / towns (i.e. Chambersburg, PA) and rural area / interstate (Mount Arlington, NJ).

Looking ahead to the remainder of 2022, it is expected 376 (38.5%) of submarkets to meet or exceed their 2019 Guest Paid RevPAR performance. Given the momentum in the second half of 2021, it’s possible that even these expectations are conservative. However, that still leaves about 60% of submarkets performing under 2019 levels in terms of Guest Paid RevPAR contribution, where we still find the majority of large metropolitan area submarkets.

In April 2022, we saw all major U.S. air carriers and most major transportation systems drop mask guidelines as a result of updated guidance from the Centers for Disease Control and Prevention and a federal court ruling. We expect this to provide an additional boost to travel, primarily in commercial segments, as more business travelers and groups start meeting in person. A Q1 2022 Deloitte study revealed many companies and organization leaders still cite time, expense and carbon emissions/sustainability as a reason to continue to curtail travel throughout 2022.

We can’t ignore the material changes the U.S. hotel industry has experienced over the last 36 months as they relate to business mix. Commercial strategy teams must keep this in mind as they plan ahead for 2023 and beyond. Leisure travel will remain on the upswing and likely a cornerstone of a successful business mix in most market types. Commercial will find its way back to large metropolitan areas and mid-sized city market types as business travelers get comfortable on the road again and corporate leaders recognize the contribution of in-person meetings to business growth.