Revenue Strategy: Investing in Your Hotel’s Optimal Channel Mix The Billboard Effect is Dead, Rate...

Published Articles

BY MARK LOMANNO, PARTNER & SENIOR ADVISOR, KALIBRI LABS

While much changed for the US lodging industry following the pandemic, two of the more interesting shifts in consumer behavior began to occur during the early recovery stages from the pandemic and remain now that the industry is almost fully recovered

Those two are dramatic shift in day of week occupancy performance and average length of stay (LOS) changes. While these may be two different topics they are interrelated, as the increase in the LOS played a huge role in the changes in day of week occupancy.

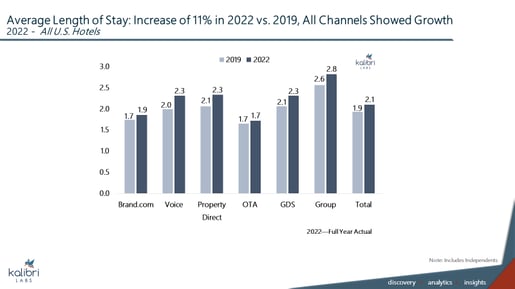

In 2019 the average length of stay (ALOS) for guests in U.S hotels was about 1.9 nights, meaning the majority of guest stays had to be for 1 night. In fact, over 64% of all hotel stays in that year were for just one night. In 2022 the average length of stay (ALOS) jumped dramatically to 2.1 nights; however, the majority of stays were again for just one night, coming in at about 62%. When thinking about customer mix in two very broad categories, one being commercial (primarily business and group stays) and the other defined as leisure, the obvious conclusion is that the majority of the increase in LOS can be attributed to longer stay patterns by transient leisure travelers. As such, customer demand on what are referred to as the shoulder days (Thursday and Sunday) was much stronger than any point pre-pandemic.

When looking at the average LOS stay by which channel the reservation was booked reveals that every booking channel with the exception of OTA resulted in longer stays by the guest. The biggest gain was in voice bookings which had a 0.3 point jump. This is not surprising as during the early stages of the recovery, which began to occur in earnest during the 2nd quarter of 2022, hotel guests were much more likely to want to receive voice verification of their stay and the amenities that would be available to them as many hotels were either temporary closed or had limited services available.

While the 0.2-point increase reported at the national level in the ALOS may not seem dramatic, from an overall industry performance standpoint that change had significant implications. After making some informed assumptions about supply and tying that to occupancy levels for each of the two years in question, a higher ALOS means that there were, in fact, fewer guests check-ins in 2022, when compared to 2019. This implies that if demand was measured by the number of guests traveling, current demand levels are actually a bit weaker than the performance results would indicate. This longer LOS when combined with especially strong industry ADR performance, resulted in RevPar levels for most industry segments and markets well above the previous highs reached in 2019. However, while RevPAR exceeded pre-pandemic levels in 2022, actual guest demand for hotel rooms was weaker than the revenue growth would imply because there were fewer actual guests in hotels.

One way to think about the impact of ALOS on industry performance is that assuming one of the two factors that determine occupancy (supply) remains static, a longer ALOS must result in fewer check-ins to achieve the same demand levels. Conversely, a shorter ALOS has the opposite effect, meaning that more check-ins are required to maintain consistent demand levels.

The question facing the industry is whether this increase in average length of stay (ALOS) is an outlier due to a change in immediate post pandemic behavior or a permanent reset in stay behavior that will persist going forward. Should the ALOS remain at this inflated level as the expected return in both transient business travelers and group return comes closer to former levels, it would be a very positive long-term development for the hotel industry. Conversely, should LOS patterns return to historical levels, the current demand shortfall would be a bit exasperated.

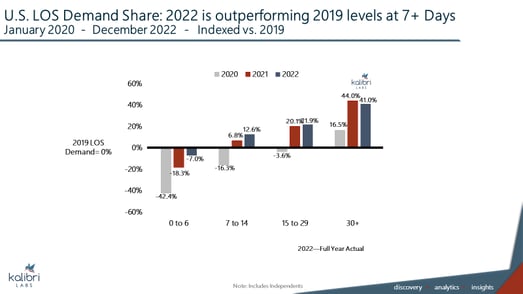

As the number of stays of one night did not materially change between 2019 and 2022, a longer average LOS could only have resulted if there was an increase in extended stays. As such, stays of 7 nights or more reflected the largest increase in percentage room night growth in 2022. While gains were reported by all longer extended stays, the biggest gain was shown in the 7–14-night stays, clearly benefiting extended stay hotels more than other property types.

However, to keep this in perspective, room revenue for all stays in the U.S of 7 or more nights in 2022 was still a relatively small percentage of total US lodging revenue in 2020, representing just under 20% of total guest spend. If this trend were to continue, the importance of this segment will continue to increase.