As the end of 2024 nears, and we wrap up planning for 2025, it’s crucial we don’t lose sight of one...

Blog

By Jeremy Gilston - May 6th, 2020

With a staggering number of confirmed COVID-19 cases across the globe, which grows by the hour, it is clear that the pandemic’s impact is widespread and likely long-term. Industries are evolving in real-time to meet the new needs of the marketplace.

Hotel real estate and investment stakeholders can use data to navigate the recovery from the COVID-19 pandemic, but the cause of this downturn is unique, such that data from past recessions will be less useful than it was in previous downturns as an indicator of recovery.

The nature of this downturn suggests the hotel industry recovery will vary significantly by type of business. For example, corporate business travel may be slow in coming back due to concerns about the health risk to their staff and tightening budgets. Additionally, some portion of corporate business travel may not return at all given the success of business conducted remotely while sheltering in place. Group business will likely have state or local restrictions on gatherings for many months to come. Leisure-oriented business booked through OTA’s is already showing signs of a recovery as of the week ending April 24th.

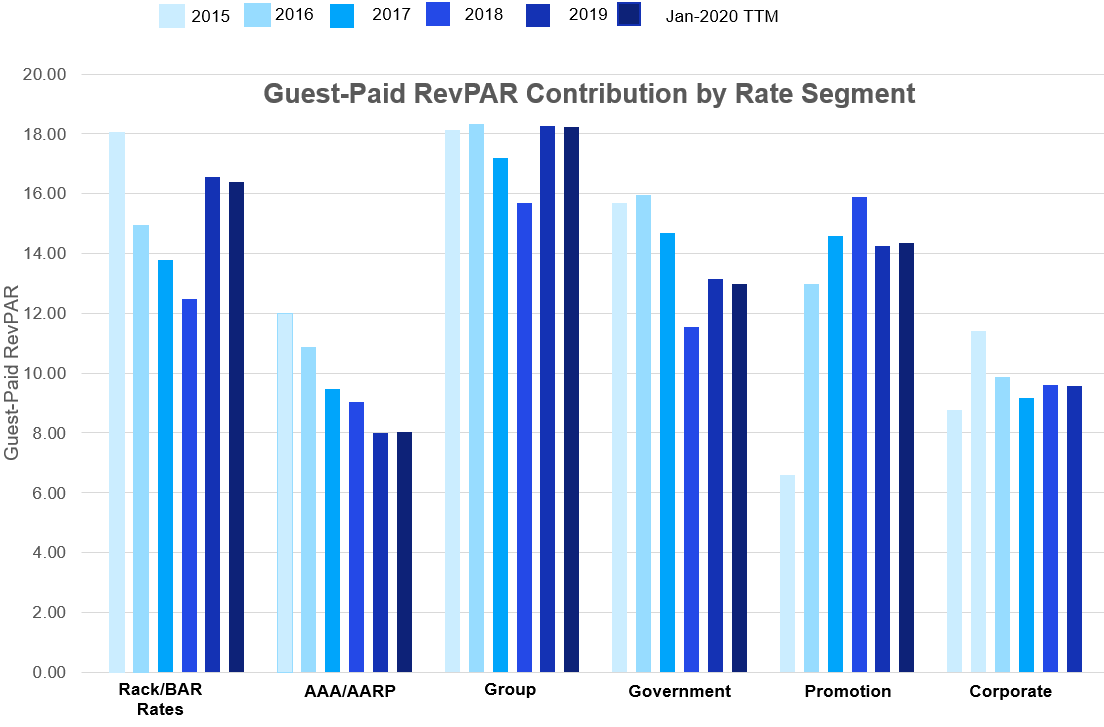

Simply looking in the rear-view mirror for RevPAR of a hotel, a comp set, or a market will be too limited a view to navigate this current challenge. Fully profiling the history and reviewing current information by demand profile will lead to better-informed decisions

The best-informed stakeholders will seek the full composition of RevPAR to more accurately project the future. Given some of these impact and recovery factors, what data is available and how should it be applied to upcoming decisions?

Short Term: Segmentation Data

With the immediate halt of international travel and a significant decline in domestic travel, many hotels do not have adequate cash flows to cover operating costs. And for those who do, debt payments are becoming an issue. As a result, there are two short-term decisions to make:

-

What financing options are available to me?

-

What is the threshold at which my hotel must cease operations?

As cash flow is a result of operating income and expenses, having access to detailed hotel segmentation data can provide the borrower and the lender a more accurate basis for projections.

The group-heavy upper tier hotels in major metro areas are likely to experience a slower recovery, while extended stay and mid and lower tier hotels in secondary or tertiary markets are less impacted and more likely to recover sooner. Detailed segmentation, broken out into rate categories, provides crucial insight into a given subject hotel, grouping of hotels, and/or market to inform the short-term decisions around recovery planning.

Source: Kalibri Labs Trendline Report

Access to this detailed composition of RevPAR will allow an underwriter to project a more realistic scenario going forward that can lead to favorable refinancing and/or debt restructuring terms. Lenders are looking to mitigate risk, so it is a well-regarded step when a borrower takes the initiative to build the most accurate and data-driven recovery scenario(s) possible.

Additionally, this segmentation-based underwriting analysis can inform an owner and/or operator’s path to produce revenue, manage operating expenses, and find realistic ways keep the hotel operation running during these challenging times.

Mid Term: Market Impact and Recovery Scenarios

Most real estate and investment stakeholders have already assessed the situation and begun the process of refinancing and/or closing floors or shuttering hotels entirely. However, many are seeking loans, finding new sources of capital or partners, or completely liquidating through a sale. These are the types of mid-term decisions that require insight into the recovery patterns. So the next questions become:

-

What is the severity and duration of the weak lodging demand?

-

Which markets will return first?

-

How can an asset be positioned to recover as quickly as possible?

Because this recovery will vary by type of business, the historical mix of demand will strongly influence any hotel’s expected recovery. AAA/AARP customers for example, who represent an older cohort of travelers, may take years to confidently travel again. On the other hand, the younger set of leisure travelers booking through Online Travel Agencies (OTAs) may bounce back quicker as the pent-up demand combined with promotional activity may get them back on the road this summer.

The mix of business over time impacts the booking cost per occupied room, another powerful decision-making metric. Continuing with AAA/AARP vs OTA: FY-2019 Total U.S. performance, AAA/AARP occupied room nights cost hotels about $9 to acquire, as compared to ~$22 for OTA room nights.

.png)

Source: Kalibri Labs Market Impact:Recovery Analysis

The sample Market Impact:Recovery Analysis below examines three recovery scenarios: 18 months, 36 months, and 48 months. These three scenarios are broken out into upper, middle and lower hotel tiers as well as by rate category to help stakeholders understand key recovery metrics by month and year:

These models exist for the total U.S. and for 60+ markets and are based on:

-

Past and current customer rate category demand patterns

-

Impact and Recovery timelines derived from historical hotel demand, CBRE Hotel Horizons quarterly forecasts, and interviews with hotel brands, owners, and operators

-

Impact timelines by market by property type categories

Continuing with the AAA/AARP vs OTA example: as of April 2020, the total U.S. 18-month recovery scenario projects that by September 2020, AAA/AARP revenue will be 40% lower than September 2019 levels, as compared to Merchant Model OTA revenue (like Expedia), which will only be 10% below. Once again, knowing the business mix that will constitute the hotel’s RevPAR will make a material difference to the recovery timeline and ultimately cash flow projections. Having these guidelines of several recovery scenarios supports more accurate analysis for any given hotel.

Long Term: Traditional Opportunity Indicators

Given the likely reduction in competition, there may be good opportunities for those in a stronger cash position. To capitalize on these, investors will still need to consider:

-

Which markets are favorable?

-

Which asset classes are favorable?

-

Is new development still an option?

Traditional underwriting will remain the playbook for these hotel opportunities; understanding the profile of the historical demand in a market will significantly enhance the analysis. Although new development opportunities may dwindle until construction loans become easier to secure and construction resumes, acquisitions and repositioning will remain enticing.

In addition to the example displayed above for assessing an asset of existing interest, rate category or channel information is also the key to power a focused market opportunity and acquisition strategy:

-

A market that had an excess of extended stay demand being accommodated at non-extended stay hotels will still be ripe for additional extended stay supply.

-

A submarket where 60%+ of bookings were made by brand-affiliated guests will still be a good opportunity to acquire an underperforming independent hotel and add a brand flag.

-

A hotel that has maintained high occupancy early in the COVID-19 recovery with a relatively low cost of customer acquisition will still be a cash cow.

Read this article to learn more about four metrics that strengthen traditional underwriting.

Key Takeaways

Assets may change hands, but hotel real estate is not going anywhere. Certainly, many aspects of the hotel industry will change, but unlike retail or financial services, the hospitality experience can not shift to a digital/virtual model. Travel has become a necessity, no longer a luxury; the hotel industry will recover.

Real estate investors can mitigate the short term, prepare for the mid term, and take advantage of the long term. But it will require more surgical and data-driven evaluation of the demand than ever before. Those who embrace critical new data and analytical tools will excel as they navigate the upcoming recovery cycle.