By Mark Lomanno

Published Articles

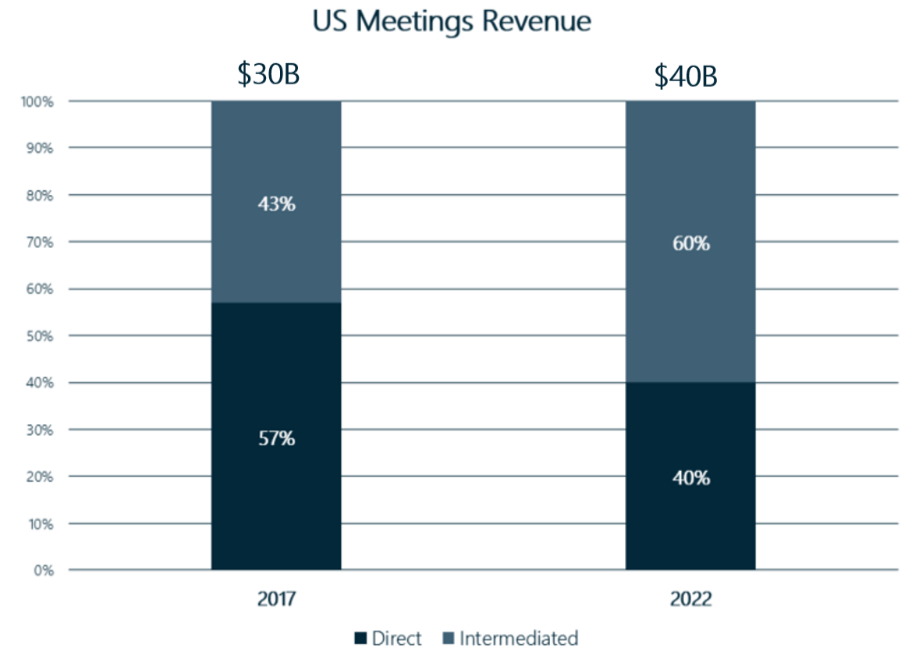

The U.S. meetings industry generates approximately $30B in hotel room revenue with another $110B estimated in ancillary spend including catered food and beverage, AV, ground transportation and other services

Yet, surprisingly, a relatively small number of hotels can take large groups. In fact, based on analysis of the Kalibri Labs census database, in looking at the U.S. in total, just over 10% of hotels have over 160 rooms and just over 7% have 8,000 sq. ft. of meeting space or more.

While all hotel segments participate in the groups and meetings business, smaller meetings differ in terms of complexity related to meeting space and ancillary services, the way they are booked and serviced may vary considerably from the larger meetings. Despite the differences, the process to book and execute meetings business has been characterized by many parties involved to be cumbersome and inefficient. The costs associated with this execution have risen dramatically over the last five years with a variety of third parties providing services at various points along the process.

Although there are a large number of parties involved in the groups and meetings booking process, it hasn’t fundamentally changed in 40 years. It is cumbersome for the meeting planner as well as the hotel or supplier serving the guests. A vendor ecosystem has grown around this static process with various service providers assisting along the way, charging fees and shifting the value around from the traditional legacy model. In the legacy model the host organization paid the venue for all aspects of the meeting whereas now the value of the meeting is now diffused across the many providers of services in the chain and the overall cost to conduct a meeting has risen dramatically. There are three primary players in the process: (1) the host who decides they want to have a meeting, (2) the meeting planner who runs the process of executing on that meeting and (3) the supplier(s) who provides services in the execution of the meeting such as hotels, CVBs, AV companies, florists and ground operators. Added to the primary players are the secondary ones who have entered to support one of the primary three. It is this secondary market that has been the main source of incremental costs.

While automation has resulted in increased efficiency in many other spaces, it has not substantially improved the ease of groups and meetings booking despite the introduction of technology over the last 5-10 years. There are certainly areas that have been made easier but there are still many aspects that are tedious and cumbersome and because of the many players involved, it may be more difficult to leverage technology across all parties. The meeting host, meeting planner and hotel or event supplier all find the process complicated and labor intensive with many pain points. Ultimately, as the costs have risen within this fragmented ecosystem, so too have questions about ways to streamline the process.

Since the 2008-09 recession, the groups & meetings business has rebounded and there have been many online platforms that have emerged to support this business, as well as offline consultants that assist corporations and associations in their sourcing. In the online platforms, much of the focus has been on identifying and fielding venue options and the offline support has been largely in sourcing and contracting the events. To enable bookings, the platforms would require access to inventory for both guest rooms and function space at a minimum and ideally, they would also offer room rates and catering options to allow some meetings to be contracted entirely online. The complexity involved in this has been the primary reason for delays in the development and adoption of this technology. Traditionally, control of hotel meeting space has been decentralized at the property level and building connectivity to it for external users to gain direct access has only been initiated in the last few years.

While much of the automation for groups and meetings has facilitated parts of the process for meeting planners, it has come at the expense of suppliers and the fragmentation still poses problems for all. For instance, companies provide tools for meeting planners to review venue options by automating the distribution of requests for proposal (RFPs), while this may ease the meeting planner’s job, it can cause hotels to incur high labor costs fielding large volumes of requests with a varied range of lead quality and declining conversion rates. To automate more of the process, some companies like Cvent have indicated an interest in supplementing their current functionality to include completed bookings, and Expedia has tested the use of their platform for individual bookings for small groups that don’t involve meeting space. There are also many new players like Groupize, BookingTek and HotelPlanner that have gone down the path of offering either white label solutions for a hotel’s branded website to enable online bookings or for independents to make their hotels available in a larger multi-brand platform. The traction in multi-brand booking capability is still limited, likely due to the need for broader access to meeting space that can be offered through a user-friendly interface for consumers.

While some of the concerns in this ecosystem involve control over the meeting space inventory, there is also a high level of concern around the cost of sales brought on by additional vendors.

Many hotels pay traditional offline third-party intermediaries working on behalf of meeting hosts for an estimated 40-50% of their meeting business. In the 1980s and 1990s, corporations and associations had their own internal meeting planners and worked directly with hotels to execute events. Over the last ten years, owing to an accelerated transition to third party meeting planners, many of these associations and corporations were able to reduce their internal meeting planning budgets to a minimal spending level and remove all or most of their head count in the area as the third-party planners took on this task and asked the hotels to pay them for it. In fact, third-party planners share some of the fees they earn with their association or corporate clients to reduce the cost of the meeting. Because of the shift to third-party meeting planners, it can create distance between the meeting hosts and the venue which is in sharp contrast to the direct relationship that was prevalent for many years between the end user corporate or association account and the hotel teams.

This disruption of a previously direct relationship may diminish a hotel’s ability to understand an account’s requirements in order to provide better and more personalized services. There are also costs associated with the third-party economic model that are increasing and are now borne by the hotel, but used to be absorbed by the meeting host organizations.

image-block-outer-wrapper

layout-caption-below

design-layout-inline

"

data-test="image-block-inline-outer-wrapper"

>

sqs-block-image-figure

intrinsic

"

style="max-width:919px;"

>

class="image-block-wrapper"

data-animation-role="image"

data-animation-override

>

>

With so many parties involved at various stages in the process from sourcing to execution, each asks for a cut of the revenue or added transaction fees. It is estimated that, at a minimum, over 40% of group business is intermediated at the point of sourcing and some at many points before execution. The level of cost rises with more intermediaries participating and with more meetings of different types and sizes subject to commission and other fees. Across the U.S. hotel industry, Kalibri Labs estimates these costs in 2017 will be approximately $3.4B to $4B and as more third parties emerge and more business is subject to intermediation, this cost could potentially double by 2022.

Based on 2017 group rooms revenue of $30B industry-wide, the cost of intermediary commissions alone was estimated at $1.3B. This is based on 43% of group rooms revenue being intermediated at a commission rate of 10%. This does not include all other aspects of the ecosystem that may involve eChannel advertising, group block reservation processing and other technology related costs increasing the total to closer to $3.4-$4B. As group booking intermediation evolves further into a combination of third-party planners and third-party technology the rate of intermediation will grow. In 2022, with an estimated $40B in group room revenue, expectations of two-third intermediation and costs closer to 15-20% of revenue, the potential industry cost could reach closer to $8-10B.