By: Cindy Estis Green

Blog

By: Cindy Estis Green, CEO & Co-Founder, and Matt Carrier, Director of Revenue Strategy & Account Management

Featured in the Fall 2016 issue of HFTPs "The Bottomline".

An excerpt from "Demystifying the Digital Marketplace: Spotlight on the Hospitality Industry"

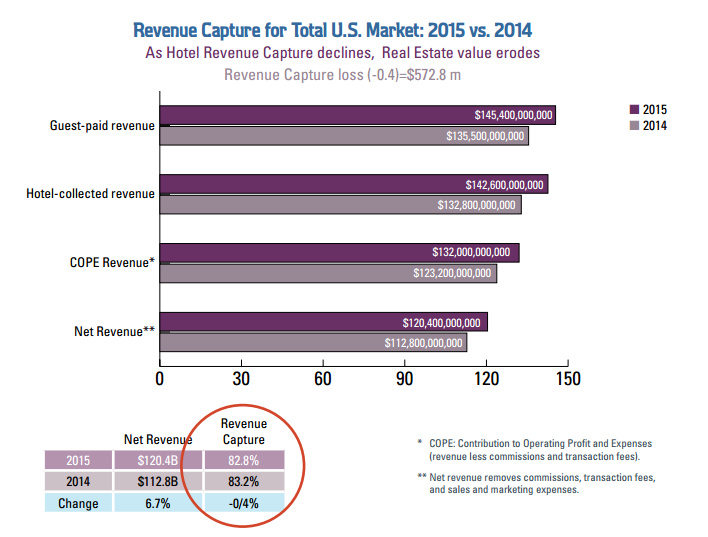

The digital marketplace has undergone a significant amount of change in the intervening years since Distribution Channel Analysis: A Guide for Hotels was published in 2012. What follows below is an excerpt from the follow-up to that book, Demystifying the Digital Marketplace: Spotlight on the Hospitality Industry co-authored by Cindy Estis Green and Mark Lomanno. In 2015 U.S. hotels paid approximately $25 billion in overall customer acquisition costs on guest paid revenue of $145.4 billion. This guest paid revenue grew year over year, from $135.5 billion in 2014 to $145.4 billion in 2015. Guest paid revenue represents the revenue a guest actually paid for a hotel room including any commissions that were retained at the point of booking by a net/merchant intermediary or wholesaler. Despite this, the revenue capture figure for the industry in the U.S. declined by .4 percent over that same period. Revenue capture measures the percentage of guest paid revenue that is retained after all customer acquisition costs are paid. The revenue capture decline, from 83.2 percent in 2014 to 82.8 percent in 2015, represented almost $600 million in revenue that, if it had been retained, would have contributed directly to net operating income and the hotel’s return on investment. Using an 8 percent capitalization rate, this additional cost of $600 million reduced the asset value of the overall hotel industry by at least $7.5 billion in 2015. That equates to $1.7 billion in real estate asset erosion for every 10th of a point lost in revenue capture.

With this impact of distribution costs in mind and following a deep dive into the travel distribution landscape, three primary themes have emerged:

1. Hotels are exploring new techniques for implementing revenue strategy. An abundance of new online models has driven an imperative for hotels to shift from traditional, analog operating methods to a focus on digital.

Current operating methods are costly and deployment is inefficient. This fact is evidenced by the rate of third-party commission growth rising at twice the rate of revenue growth. Hotels previously tried to be available “on every shelf,” but most have realized at this point that it costs too much to be prominent in every distribution channel and the dominance of third party intermediaries in the consumer path can undermine the relationship between hotel and consumer.

Hotels will always have the opportunity to build a relationship during the actual stay experience, but risk losing out on the connection made through inspiration, information gathering and booking phases of the travel journey. Third party intermediaries are focused on developing their own customer bonds and have little incentive to facilitate the relationship between a hotel and their shared customer.

Therefore, in spite of a mutual dependence between hotels and third parties, a sense of competition arises for “owning the customer relationship.” Two critical components of revenue strategy involve managing to a hotel’s optimal channel mix, including close tracking of acquisition costs, and differentiating the guest experience during the stay, as well as in pre- and post- stay contact.

Every single booking, no matter the source, comes with a price tag. A hotel will never get all of its bookings from a single channel and so hotels must work to identify and manage to an optimal channel mix. At the hotel level, managing costs is not simply about negotiating a better deal with a channel vendor such as an OTA. It’s about understanding the profile of demand in a hotel’s market, the costs associated with getting that demand, and then proactively managing to an optimal channel mix, optimal because it yields the highest net revenue and profit contribution.

2. The legacy OTA model is threatened while apps and metasearch are gaining traction by providing consumers a more convenient and seamless experience across air, car, hotel and other components of travel. The legacy OTA model once assisted consumers by narrowing down lists of hundreds of hotels while still offering a wide range of options. A number of new models point to a next generation consumer interface. With metasearch and social sites (like TripAdvisor and Facebook), along with some new apps (like Google Trips) now seamlessly integrating many elements of travel, the evolution toward a curated consumer experience is underway. In the meantime, some foundations of the traditional OTA model have been challenged.

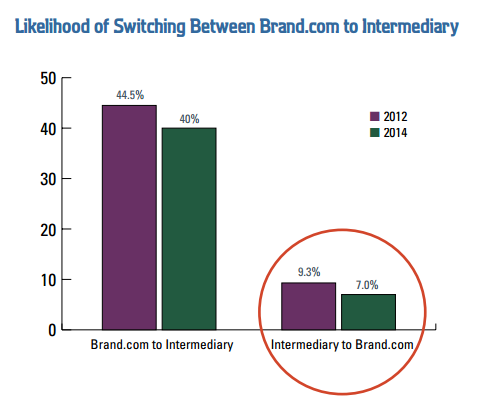

Through rigorous research on consumer clickstream data, the “billboard effect” was dismissed as a dead concept. The claim had been that OTAs drove multiple brand. com bookings for each one booked directly on the OTA site. However, a 2015 research study sponsored by the Consumer Innovation Forum (CIF), an American Hotel & Lodging Association committee focused on the education and research of the hospitality industry’s digital and distribution space, proved there is barely any lift in brand.com bookings as a result of visits to traditional OTAs. Consumers had only a 7 percent likelihood of visiting a brand. com site after an intermediary.

Conditions that locked up hotel inventory and rates for third parties such as rate parity and last room availability are dissolving, whether from European regulators in multiple countries or changes in large chain agreements, thereby paving the way for greater autonomy by hotels and smaller third party distributors. These changes will ultimately result in a more open and competitive marketplace.

3. New entrants spell disruption for select customer segments. Corporate travel has long relied upon legacy travel management companies handling the larger managed travel accounts, in contrast to a high degree of fragmentation on the lightly managed and unmanaged business travel. New developments are likely to force change in the traditional RFP process for corporate accounts — such as rate scanning with auto-cancel and rebook capability up until day of arrival, reward and incentive programs for travelers to self-police their own spending, aggressive moves by third parties to aggregate the lightly managed accounts, along with consolidation by hotel chains who don’t participate in annual rate bids. Corporate account activity will further be diverted by the aggregation of home and vacation rental markets, which will also create supply spikes during leisure high demand periods.

The groups and meetings market is also ripe for disruption. The last five years have seen extensive offline third party intermediation, but no one has yet managed to aggregate this demand by offering a compelling online venue for casual or professional meeting planners to shop and book. Historically, the booking of groups and meetings has been inefficient and costly, but indications are that the next three to five years will bring new options for this segment which may finally streamline a highly inefficient process with reduced costs and an improved experience for the consumer.

With these major industry sea changes in mind it is clear that hotels must be more focused than ever on driving profitability through a focus on Net Revenue. These three themes, along with many more, are explored throughout Parts 1–3 of Demystifying the Digital Marketplace: Spotlight on the Hospitality Industry. HFTP is a sponsor of the report, and a copy is available now to HFTP members (password: HFTP2016).